Restauranteurs are passionate about their business, but many only see the greatest risk to their business as survival. Stats of restaurant failure are over-exaggerated, but believed by everyone. Myths of 90% failure rate prevail in the industry consciousness. The truth is: closer to 60% will fail within the first 3 years. That number is not much different than most businesses.

The myth of impending business failure keeps restaurant owners from looking at their true risks. And it’s these risks that insurance for restaurant owners can solve.

The investment in a good insurance product is a major factor in a sustainable restaurant business.

Most coverages a restaurant owner needs can be found in a BOP (Business Owner Policy). In fact, many insurance companies have created BOPs specifically for this niche. These restaurant insurance programs are comprehensive but won’t include everything needed to protect a restaurant business.

Let’s examine the coverages inside the Restaurant BOP and then discuss the additional coverages needed for a restaurant to be fully secure.

What is a Restaurant BOP?

The Business Owner Policy (BOP) is a streamlined package commercial product that combines both General Liability and Property Insurance. The beauty of the BOP is that the coverage pieces are in place for you without you having to build the policy yourself.

Not only does this save time, but gives you confidence that you didn’t miss an important coverage. By packaging the coverages together, customers save money as well. The premium would be much higher if you bought each coverage separately.

Just because BOPs are self-contained doesn’t mean they cannot be modified. Most companies have created BOPs around various niches or industries. These will provide the most common coverages needed by those industries.

Even with these coverage enhancements, a great agent should do a full risk analysis and make sure further endorsements shouldn’t be added to protect the client from any gaps in coverage.

Restaurant BOP Coverages

When buying insurance for restaurant businesses, the Business Owner Policy is an attractive choice for its coverage bundling. The Restaurant BOP insurance covers three major items:

- Damage to business property

- Injuries to restaurant patrons or their property damage

- Advertising injuries such as slander

Here’s what these coverages look like in your average restaurant.

1. Damage to Business Property

Property Examples

- Inventory including perishable food

- Kitchen equipment

- The building (if you own it)

- Improvements and betterments (if you rent)

Potential Hazards Covered

- Fire – even if it is not started in your building but spreads to you from another building

- Vandalism & theft

- Weather damage

- Burst pipes

- Will not protect against flood

2. Customer Injury

Examples of customer injuries can include:

- Slip and fall injuries

- Food poisoning

- Server spills a drink on a customer’s phone or laptop

Liability coverage will cover court costs, attorney fees, and other legal expenses.

BOP vs General Liability

A BOP (Business Owner Policy) will cover both property and liability. A General Liability policy only covers liability.

3. Advertising Injury

This can be confusing to most business owners, and one you need to help clarify the potential risk. For example, if an employee writes a negative review about a competing restaurant, the other business could potentially sue for libel.

Useful Restaurant Endorsements

Many BOPs designed for restaurants will include endorsements specific to that niche. However, there are some coverages that are often separate. These are the most common not to be included in a restaurant BOP.

Liquor Liability

If a restaurant serves alcohol, this coverage is a must-have and will protect the owner from a wide range of liquor-related lawsuits. If an intoxicated customer gets hurt in a fight or hurts someone on premises, this will protect the business. The business will also be protected if the customer drives home and causes an accident. Maybe an employee mistakenly serves an underage person and trouble ensues—they will be covered under this endorsement.

Business Interruption

Closure due to damages sustained from a property hazard such as a fire or natural disaster can damage the business income. Business interruption protects against loss of income during times the business had to be shut down.

Furthermore, the restaurant may be dependent on a third party to deliver goods to operate. If the third party sustains a loss that prevents them from delivering, this could also impact a restaurant’s income.

Cyber Liability

Restaurants collect very sensitive information, like customers’ credit card information, employees’ Social Security numbers, and employee banking information. If that data is stolen, the business can become liable and have its reputation damaged. Cyber Liability protects against such losses.

Food Spoilage or Contamination

The core of a restaurant’s product is food. If the food is bad, the financial loss is imminent. Protecting this source of their income is paramount. The most likely cause of spoilage is power outages or faulty equipment, but contamination can be tricky to diagnose. When contamination happens, there is no salvaging the product.

Most industries can skip this coverage, but not the restaurant industry. Remember: this coverage only reimburses product damage and not potential lawsuits from sick clients.

Equipment Breakdown

Equipment breakdown will cover losses from power surges, mechanical breakdown, motor burnout, etc. Restaurants depend on several large pieces of equipment that can impact the business if broken. Not only is the equipment itself covered, but business income and spoilage are part of this coverage.

Even if a restaurant leases equipment, they need this coverage. They may not need to protect the actual machinery, but do need protection against lost income when equipment fails.

Outdoor Signs

This coverage is often covered in some BOPs, but not always. Restaurants can spend a significant amount on signage. Signs need protection against hail, windstorm, lightning, and even vandalism.

Employee Dishonesty

This happens too often in most restaurants. Usually, employee theft begins with small amounts but creates boldness that creates bigger damages over time. While every business needs to be vigilant with employee behavior, employee theft does occur, and they need to protect themselves.

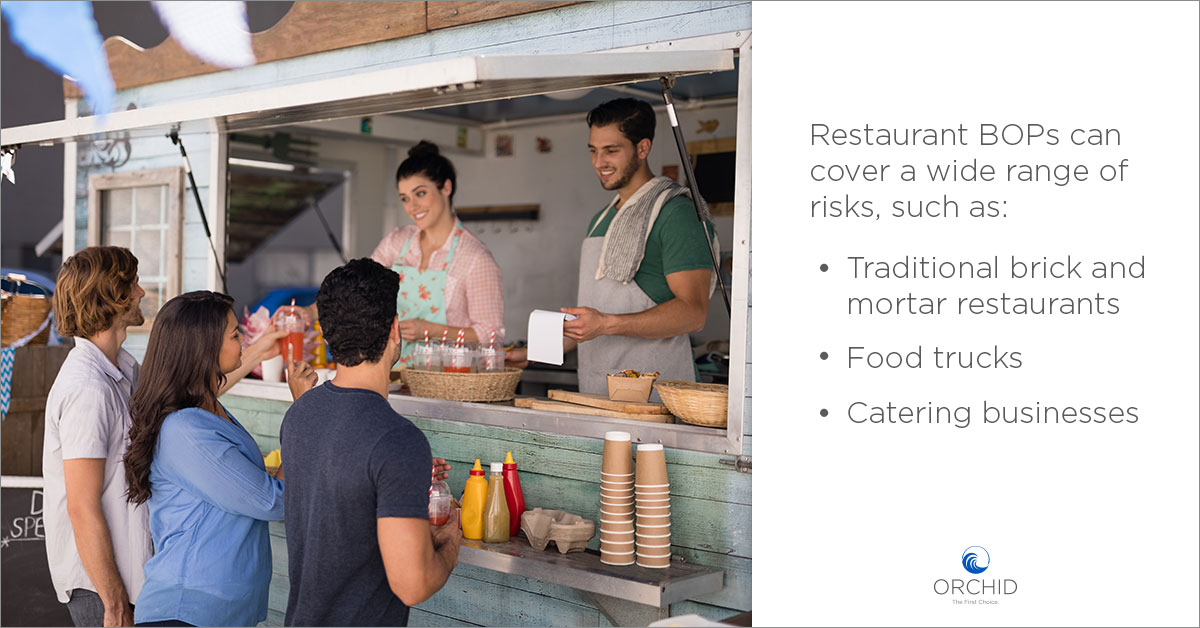

Eligible Restaurant Clients

Restaurant BOPs can cover a broad range of risks, including typical brick and mortar restaurants, as well as food trucks and catering businesses.

The types of restaurants that are eligible are bigger than you might expect as well. Most BOPs can handle large physical operations as well as those that generate $8-9 million in gross sales.

Bottom Line

As an agent, it is helpful to have product built for your niches. This is true for the restaurant industry.

Even a robust BOP fully endorsed can be missing coverage such as Workers Comp, Commercial Auto, and EPLI (employment practice liability insurance).

As an agent, you still need to examine each package you present to your customer and truly understand their risks. But you do have resources that can protect your current and potential clients.

For more information on restaurant BOPs, contact Orchid Insurance at 772-226-5546 ext. 239.