You may already be familiar with HO3 policies as they are the most commonly used homeowner’s insurance policies, but it’s important to understand there are other options out there. Here we’ll review HO3 policies in detail before comparing them to their lesser known sibling, the HO5.

HO3 Homeowners Policies

HO3 policies are the most commonly used because they are the most applicable to everyone and are generally considered to be the minimum acceptable coverage when obtaining a mortgage.

An HO3 typically has 5 coverages: A, B, C, D and E.

- Coverage A: This covers the actual home you live in and any attached structures, like a garage. Your home is usually covered on an open peril basis. This means that your home is insured for any event unless specifically stated otherwise. A deck or porch may also be considered an attached structure and be covered here. It’s important to clarify with your agent what is or isn’t considered an attached structure.

- Coverage B: This covers other structures on your property, such as things that are unattached to your home. Common items covered here are pools, sheds, fences, and detached garages. Typically, these other structures are insured for up to 10% of your Coverage A amount. So, if your home is insured for $200,000, your other structures would be covered up to $20,000. You can increase this coverage if you’d like a coverage amount more than 10%.

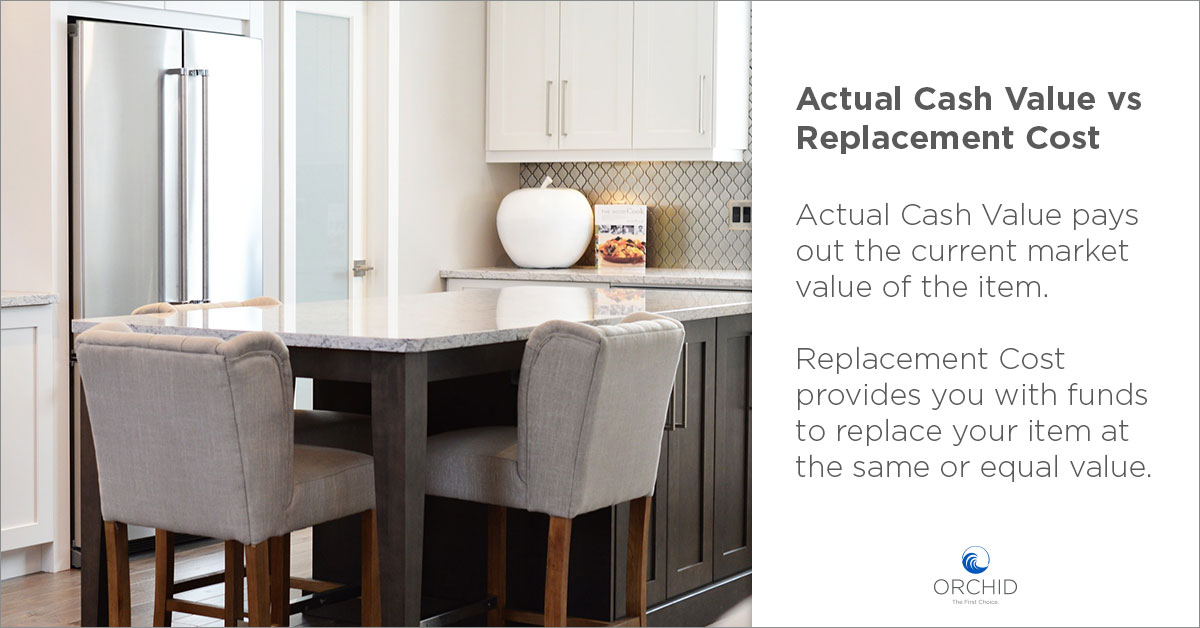

- Coverage C: This covers the contents of your home, otherwise known as personal property. Reimbursements for damaged items are usually paid in actual cash value. This means depreciation is taken into account and you will only be paid the amount your items would sell for on the market. Orchid is unique in which all our policies cover contents on a replacement cost basis. Unlike your home, which is covered for open perils, your contents are covered for named perils only. This means your contents are only insured for events specifically listed on your policy. If it’s not listed, it’s not covered.

- Coverage D: This covers you if your home becomes uninhabitable. It’s commonly referred to as loss of use coverage. This will cover the costs of staying in a hotel and any additional living expenses you incur while your home is uninhabitable. This coverage is usually on a named peril basis as well and is either limited to a certain period of time or 10% of Coverage A.

- Coverage E: This is the personal liability portion of your Homeowners Policy. You’ll be covered for a variety of situations where you’d be at fault. This will cover the cost of a lawyer to defend you and pay the damages you’re responsible for. Orchid’s liability coverage begins at $100,000.

HO5 Homeowners Insurance

HO5 policies serve the same purpose as HO3s but are different in a few key ways.

- The first difference between HO3 and HO5 policies is eligibility. HO3 policies are available to all home types and it is up to the insurance company whether to accept the application for coverage. HO5 policies are only available to newer homes in areas with a low risk of natural disasters, crime, and other perils that could cause losses.

- Coverage C: HO5 policies cover the contents of your home on an open peril basis. This means your items are protected in any event unless specifically stated otherwise. On an HO3 policy, your items are only covered for specific events, leaving holes in your coverage. There is also a difference in how you are reimbursed for your damaged items. HO5 policies cover your contents at replacement cost. This means you’ll be paid enough money to buy a new item. An HO3 policy pays you actual cash value for your contents. This takes into account depreciation and pays you the amount your items would sell for on the open market.

- HO5 policies automatically include coverages that are not covered by HO3s. For example, HO5s include extra coverage for personal property. This would have to be added to an HO3 as an endorsement.

HO3 vs HO5 Homeowners Insurance

In general, HO5 homeowner policies are more comprehensive than HO3s.

They remove many of the limitations of HO3s, expand on existing coverages, and add entirely new coverages. Most of the time HO5 policies are priced in the same ballpark as HO3s, offering additional peace of mind for a similar price.

If you live in a safe area, have many high value items in your home, or just want to eliminate some of the holes in your coverage, an HO5 homeowners policy might be right for you.

Ask your insurance agent about Orchid Insurance homeowners policies.